Prospects for a Central Bank Digital Currency in Japan, and Three Use Scenarios for Individuals

Since FY2020, Nomura Research Institute (NRI) has held the “Study Group on the Future of Currencies and Banks”, where it has continually discussed what form a central bank digital currency (“CBDC”) in Japan might take. With a view toward achieving a clear and concrete image of such a currency, participants in the FY2022 event envisioned three examples of how individuals might use a CBDC to receive money and make payments, considering the topic with the unique characteristics of Japan in mind. What sorts of use scenarios would be conceivable in a Japan where a central bank digital currency is introduced? And what kinds of infrastructure and services would be needed to make that a reality? We posed these questions to Financial Market & Innovation Research Department members Tetsuya Inoue and Junko Ishikawa, who are well-versed in this topic.

“Cashless payments” to become widespread, even for small sums

When it comes to individuals using a CBDC to receive money and make payments, three possible use scenarios can be envisioned. The first involves the payment of funds by individuals to businesses (CtoB: Consumer-to-Business). Situations where individuals shop at a retail store or an EC site, or pay their utilities or rents, would fall under this category. Cashless payments in these kinds of cases have gradually become more commonplace, and in addition to credit cards and e-money, the use of debit cards and smartphone apps (QR codes) has also grown more widespread. While there still remains a need for cash-based payments, the use of cash has stagnated as a regular means of payment. Further, we are seeing a trend whereby payments that used to be made via bank transfer are being switched to other cashless payment methods that allow people to earn points. In fact, it is becoming more common for service charges to be imposed on the receipt and payment of deposits between financial institutions.

In recent years, we have been seeing more cases in which people use credit cards not just to purchase high-priced items in brick-and-mortar stores, but also for small-sum payments on EC sites and to pay their monthly utilities, for instance. Meanwhile, in conjunction with the growth of cashless payments among demographics such as younger generations and homemakers, the need for payment methods that do not involve credit has also been increasing. Since April 2023, it has been legal to make digital salary payments by depositing people’s salaries into digital accounts instead of traditional bank accounts, using services typically named “___ Pay”. By contrast, the cost of using cash has been rising both for users and for business operators, a fact that could conceivably spur on the use of cashless payments in the form of CtoB even further.

In the future, if a CBDC were introduced that could be used for a low service fee, we would likely see users increasingly rush to adopt it as a substitute for cash. Meanwhile, there are concerns that having the central bank itself get involved in payment services using low costs to its advantage will not only squeeze the profitability of private business operators, but also stifle innovation. An ecosystem needs to be built that is well-balanced enough to enable public and private stakeholders to reap the benefits of such a currency, including with regard to the effective leveraging of existing infrastructure. And in order to balance the protection of personal information with the use of transaction information through this sharing of roles at the same time, the scope of the information to be managed respectively by the central bank and intermediaries will need to be clarified.

Why do “paper-based payment” holdouts still account for one-third of payments?

The second use scenario involves monies paid by individuals or businesses to the national or local governments (C/BtoG: Consumer/Business to Government). This includes situations where people pay their taxes or pension premiums, or receive subsidies or benefit payments. While small payments such as pension-related payments and receipts account for a majority of such cases, large-scale payments such as public works expenses would also play an important part here.

Efforts to make payments to and receipts from the government in Japan cashless have been steadily progressing. Yet a certain amount of inefficiency still remains, such as with the paperwork processing that accounts for one-third of all payments made by individuals and businesses. Despite the availability of cashless payments, the reality is that more than a few payers still choose to make paper-based payments. At the Study Group, some commented that perhaps this was due to a problem with how information is provided to users. People do not know which payment methods are suited to which taxes, or how they should use these methods (including any procedures that need to be done ahead of time), so they end up using paper-based payments through the whole process.

Another inefficiency was also pointed out with regard to payments and receipts involving local governments. For instance, companies with offices in multiple regions face a problem whereby once they have paid their taxes to a certain municipality, they need to reorganize their information in a different format for another municipality to be able to pay taxes there. As a remedy for this, a filing system called eLTAX (a common tax payment system for local taxes) was launched in October 2019 enabling businesses to pay all their taxes en masse even for different municipalities, and this system is expected to gradually cover more areas over time. In May 2021, local authorities and local tax agencies under the jurisdiction of the Tokyo Regional Taxation Bureau announced that they would be making joint efforts to promote the spread of cashless payments.

For governments and financial institutions, the streamlining of administrative procedures is another major issue. Even if your payments and receipts have been digitalized, that does not mean that your process for identifying or authenticating the other parties involved in those payments and receipts has been fully optimized. When it comes to the massive amounts of time and costs involved in paying funds for disaster relief or for COVID-19 measures for example, overcoming these challenges is key, including those regarding provision of adequate protection to the recipients. Furthermore, with payments to and receipts from the national and local governments, the need to handle unusual cases or special provisions is likely also accelerating the increase in administrative burdens.

The payment and receipt of public funds is in many respects prescribed by laws and legal systems, and in addition to the fact that reforms cannot simply be pursued with efficiency as the sole purpose, there are other difficult problems to tackle, such as having to take great care in managing taxpayer information and other information requiring special protection. That said, with the current framework, there is considerable doubt about whether the administrative burdens being shouldered by governments and financial institutions in particular are sustainable. The use of a CBDC has the potential to be effective in overcoming these issues all at once.

With person-to-person money transfers, “financial institutions × nonbank” partnerships hold the key

The third use scenario has to do with payments and receipts between individuals either domestically or overseas (PtoP: Peer to Peer). In Japan, this would cover cases where people split the bill when dining out or at private auctions, while in the case of cross-border transactions (international exchanges), it would encompass remittances to parents or children living abroad or payments involving personal importation. Peer-to-peer payments of funds account for around $2 trillion globally, and this activity is projected to grow by 15% to 20% annually. While the absolute value of this field in Japan is not very large, it is expected to grow going forward.

In cases involving purely PtoP exchanges such as splitting a restaurant bill or sending money to family, it is often small amounts of money that are paid or received, and the key aspects are efficiency with little effort required and interoperability such that payments can be made and received even when different methods are being used. Conversely, in cases of transactions between third parties such as private auctions, things like payment security in the sense of preventing payments/receipts from being reversed at a subsequent date, the safety of having payments/receipts be reliably conducted, and user protection will be comparatively more important. This is a field where not only financial institutions but also many nonbank entities are already launching services, and the government is also actively working to encourage newcomers to get involved and trying to drive innovation through measures including easing regulations under the Payment Services Act.

By contrast, the field of PtoP also includes payments and receipts of funds that are closer to BtoC in nature. More specifically, this means payments of funds in cases where individuals purchase goods or services from privately owned stores or non-profit organizations. Compared to simple PtoP transactions, payment/receipt security and safety are all the more crucial. And for retail stores and non-profits, not only is it essential to rein in the costs required for payments/receipts and to shorten the time lag for making deposits, but it would also be more desirable to be able to use the kinds of added functionalities made possible by digitalization, such as the streamlining of orders and inventory management or improvements to interoperability.

Some at the Study Meeting also pointed out time and cost-related issues involved in sending and receiving money through financial institutions. To solve these issues, five major banks launched a PtoP money transfer service called Kotora in October 2022. Kotora uses a low-cost, small-scale settlement infrastructure to provide PtoP money transfer services of 100,000 yen or less per instance at no cost. In addition, the banks also announced their plan to roll out a tax and public fund-related service going forward. As for PtoP payments and receipts in cross-border transactions, the issues of time and costs are even more significant, but nonbank entities other than financial institutions have already begun providing their own services in this field as well, and that means that more and more low-cost, rapid payment methods are becoming available to users.

Financial institutions and nonbank entities may be competitors, but there is more than a little room for them to work well together. For instance, if financial institutions could share the user verification knowhow they have amassed with nonbank entities, it would permit those financial institutions to earn appropriate revenue while also enabling the nonbank entities to effectively prevent money laundering and other such activities. If a CBDC is introduced in the future, then in terms of striking a good balance between achieving financial stability and driving innovation, we can imagine a scenario where the only intermediaries engaged in direct transactions with the central bank are limited to financial institutions operating under stringent regulations, while all other intermediaries could be a wide range of entities.

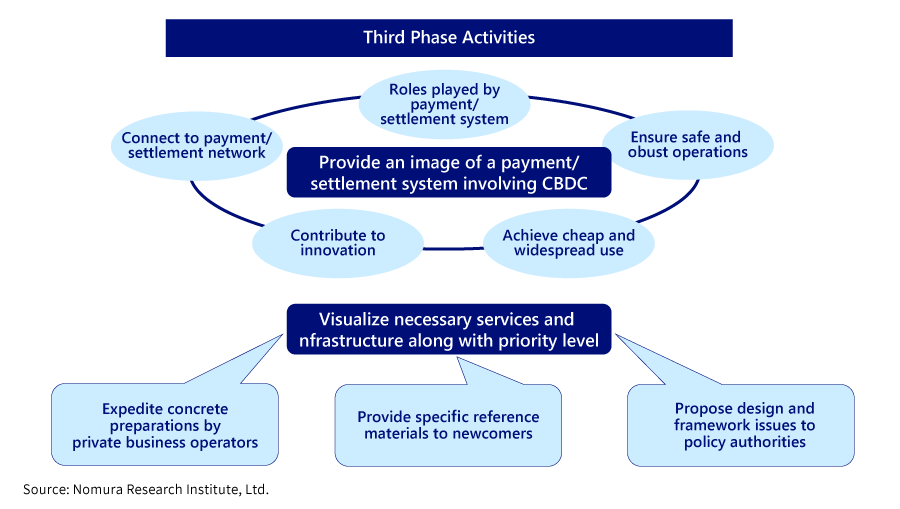

Cross-border payments involve not only issues of time and cost, but also a host of more difficult challenges such as the protection and use of transaction information among nations. For the next phase of the discussion at the Study Meeting, the plan is to expand its scope to cover payments and receipts of funds between businesses (BtoB), while also tackling how the introduction of a CBDC can help solve the challenges of cross-border payments and receipts, in the hope that this discussion will lead to a deeper understanding.

Profile

-

Tetsuya InouePortraits of Tetsuya Inoue

Financial Market & Innovation Research Department

Tetsuya Inoue capitalizes on his strong background in the central bank to conduct policy issue studies. Mr. Inoue has over twenty years of experience in surveillance of the financial markets as well as overseas activities of the Japanese banks. He also benefits from the intellectual support by his extensive network of experts at financial authorities, banks, research institutes and financial media. In 2012, Mr. Inoue launched “Banking Panel” and “Roundtable Forum between China and Japan,” expanding the scope of this research to commercial banking in Japan, as well as providing its lessons to China. He is an active writer for various economic journals, and a commentator for TV programs dedicated to experts in the financial markets.

-

Junko IshikawaPortraits of Junko Ishikawa

Senior Researcher

Financial Market & Innovation Research Department

2007-2014 Bank of Japan, International department Junko Ishikawa is a researcher in NRI’s Financial Technology and Market Research Department. She conducts European macroeconomic analyses and researches financial markets and monetary policies with a particular focus on the UK. She joined NRI in 2016 after earning an MPA degree from Columbia University’s School of International and Public Affairs. She previously worked for seven years at the Bank of Japan conducting macroeconomic analyses, researching monetary policies and preparing economic outlooks on the US, the UK, Central/Eastern Europe, Russia, Ukraine, Turkey and South American countries for Monetary Policy Meetings.

* Organization names and job titles may differ from the current version.