Prime Minister Takaichi seeks to reduce debt-to-GDP ratio with proactive fiscal policy, but...

The debt-to-GDP ratio is a key indicator of a government’s ability to repay its debts and measures the size of outstanding government debt relative to nominal GDP, which influences tax revenues. When applied to an individual, it corresponds to the ratio of personal debt to annual income and shows whether that ratio is increasing or decreasing. If the amount of debt is large relative to annual income or is steadily increasing, banks will conclude that the individual will be unable to repay his debt and will refuse to offer additional financing, forcing the person into insolvency.

Equation 1: Debt-to-GDP ratio = outstanding government debt / nominal GDP

Prime Minister Takaichi intends to increase the denominator—nominal GDP—in Equation 1 by increasing government expenditures, including investments in crisis management, thereby reducing the ratio of government debt to nominal GDP. While intuitively this may appear feasible, it is far from straightforward in practice. This is because when the government increases expenditures through the issuance of new government bonds, the numerator—outstanding government debt—also rises by an equal amount.

The increase in the denominator (nominal GDP) from higher government expenditures tends to be temporary, whereas the increase in the numerator resulting from new debt issuance is persistent and is further enlarged by the interest payments on that debt. When viewed over a somewhat longer horizon, therefore, such a policy is likely to increase the ratio of government debt to nominal GDP.

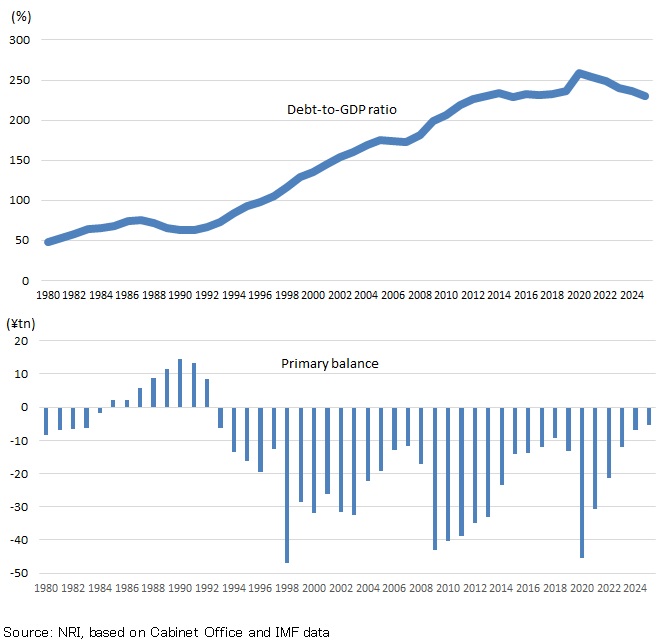

Debt-to-GDP ratio has declined somewhat over past several years

Prime Minister Takaichi plans to focus on lowering the debt-to-GDP ratio rather than on achieving a primary surplus and intends to target sustained reductions in this ratio as a fiscal consolidation objective. One reason for this approach may be the modest downward trend observed in the debt-to-GDP ratio in recent years (Figure 1).

However, this ratio tends to fluctuate significantly more than the primary balance in response to economic and financial conditions. It must therefore be assessed over a somewhat longer time horizon to provide a reliable measure of the fiscal environment. For this reason, it is less suitable as an annual target.

Reviewing the Domar condition

But starting in the 2010s, the debt-to-GDP ratio trended largely sideways despite Japan's primary deficit, and in recent years it has moved gradually lower.

This decline is attributable mostly to temporary factors—namely, the Bank of Japan's extraordinarily accommodative monetary policy and the upturn in the inflation rate.

The Domar condition states that fiscal instability will result if the nominal interest rate exceeds the nominal growth rate, whereas if the growth rate exceeds the interest rate, fiscal conditions will be stable.

Equation 2: Nominal interest rate > nominal growth rate ... Fiscal stability

Nominal interest rate < nominal growth rate ... Fiscal stability

Developing this relationship further results in the equation shown below.

Given the condition that the primary balance is in equilibrium (zero),

Equation 3: Nominal interest rate > nominal growth rate ... Rising debt-to-GDP ratio

Nominal interest rate < nominal growth rate ... Falling debt-to-GDP ratio

The primary balance is defined as revenues (excluding funds raised through government bond issuance) minus expenditures ex debt service costs (principal repayment and interest payments). Adding interest payments to this figure gives us the annual increase in outstanding government debt (excluding the effects of government asset sales, etc.). When the primary balance is in equilibrium, the increase in outstanding government debt equals the cost of interest payments on government bonds.

If these interest payments are regarded as the nominal interest rate multiplied by outstanding government debt, then the rate of growth in outstanding government debt equals the nominal interest rate. If this rate is equal to the nominal GDP growth rate, the growth rates of the numerator and denominator in Equation 1 are identical, and consequently the debt-to-GDP ratio remains unchanged.

Meanwhile, if the nominal interest rate exceeds the nominal GDP growth rate, the debt-to-GDP ratio rises, as shown in Equation 3. This adverse dynamic in the fiscal situation poses a threat to the sustainability of public finances.

Fundamental relationship: Nominal interest rate > Nominal growth rate

This pattern arises because the nominal GDP growth rate can be regarded as the economy-wide average expected rate of return, whereas the nominal interest rate incorporates various risk premia, including a liquidity premium, a credit risk premium, and a term premium.

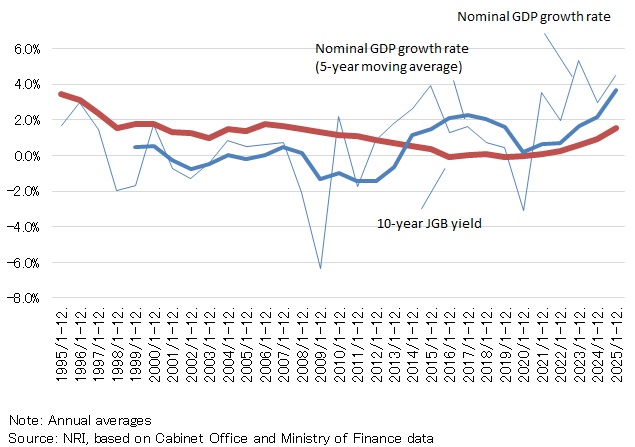

Since the first half of the 2010s, however, the 10-year JGB yield has generally remained below nominal GDP growth (Figure 2). This explains why the debt-to-GDP ratio has shifted from a sideways trend to a modest downswing despite a sustained primary deficit.

Proactive fiscal policy would prompt renewed increase in debt-to-GDP ratio

Another reason is the historic surge in prices observed since 2022. When the inflation rate picks up, the nominal GDP growth rate also rises. But if financial markets regard the inflation overshoot as a temporary phenomenon, the upside for nominal long-term interest rates—such as the 10-year JGB yield—tends to be limited.

However, the BOJ has already begun normalizing monetary policy and is phasing out the use of monetary policy to keep interest rates at artificially low levels. Furthermore, we think the price surge observed over the past several years is subsiding.

As a result, the nominal GDP growth rate will soon fall below the 10-year JGB yield. In that sort of environment, the government debt-to-GDP ratio will not decline unless there is a primary surplus, and risks to fiscal sustainability will be amplified.

If the 10-year JGB yield exceeds the nominal GDP growth rate, merely eliminating the primary deficit will not be sufficient to reduce the debt-to-GDP ratio or to enhance fiscal sustainability. A meaningful surplus would be required in that case.

The modest recent decline in the debt-to-GDP ratio is therefore not sustainable and is clearly a transitory phenomenon. For the Takaichi administration to cite this decline as grounds for continuing along an expansionary fiscal policy path would undermine confidence in fiscal policy among financial market participants. If the administration opts to implement such policy by issuing more debt and increasing the primary deficit, it could cause a marked rise in the future debt-to-GDP ratio. We think the government needs to exercise caution in this regard.

I believe the Takaichi administration should, like previous governments, firmly uphold the target of achieving and maintaining a primary surplus and accord it the highest priority.

Profile

-

Takahide KiuchiPortraits of Takahide Kiuchi

Executive Economist

Takahide Kiuchi started his career as an economist in 1987, as he joined Nomura Research Institute. His first assignment was research and forecast of Japanese economy. In 1990, he joined Nomura Research Institute Deutschland as an economist of German and European economy. In 1996, he started covering US economy in New York Office. He transferred to Nomura Securities in 2004, and four years later, he was assigned to Head of Economic Research Department and Chief Economist in 2007. He was in charge of Japanese Economy in Global Research Team. In 2012, He was nominated by Cabinet and approved by Diet as Member of the Policy Board, the committee of the highest decision making in Bank of Japan. He implemented decisions on the Bank’s important policies and operations including monetary policy for five years.

* Organization names and job titles may differ from the current version.