The February 8, 2026 elections in the lower house of the National Diet ended in a historic victory for the Liberal Democratic Party (LDP) led by Prime Minister Takaichi. When we look back on the election campaign, there was little dispute over economic policy as nearly all of the parties ran on lowering Japan’s consumption tax, and thus the debate among the parties generally seemed lacking in excitement. Even though the election is now over, one wishes that the parties would have a more vigorous discussion about what the ideal economic policy might be for improving the Japanese economy and people’s daily lives.

Is lowering the consumption tax an appropriate measure to combat inflation?

The main purpose of the parties’ proposed consumption tax cuts seems to have been one of two things: to combat inflation, as a way of supporting those in low- and middle-income brackets whose livelihoods are being squeezed by high prices; or to stimulate private consumption, which has long been stagnant.

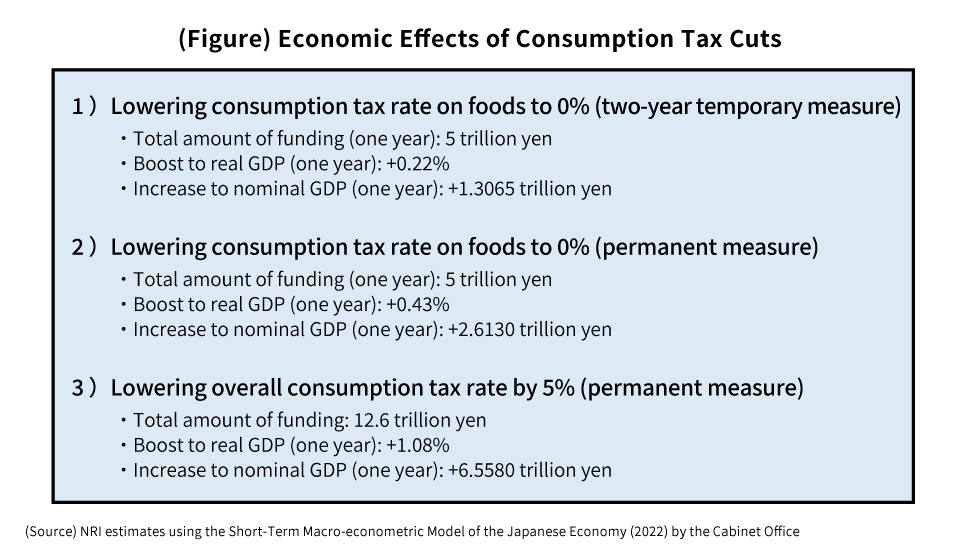

However, according to my estimates, the LDP’s proposal to eliminate the consumption tax rate on foods for two years would boost real GDP by 0.22% in a year, which is a small effect (see figure). Even if the consumption tax rate on foods were to be eliminated permanently, or the consumption tax rate overall were to be lowered, the boost to GDP would not be significant by any means. And in any of these scenarios, from the second year onward, the cuts would have hardly any effect on the real GDP growth rate.

Meanwhile, it also felt as though the funding sources proposed by the parties to cover these consumption tax cuts were generally unclear. If consumption taxes were to be cut without financial resources being fully secured, more government bonds would have to be issued, which would lead the fiscal environment to deteriorate even further.

There have already been concerns in the financial market that the Takaichi Administration’s aggressive fiscal policy measures will lead the fiscal environment to worsen, and this has eroded confidence in the nation’s finances and currency, leading to declines in the value of the yen and in bond prices (and thus to a rise in long-term interest rates). And speculation that the consumption tax rate will be cut could push those trends in the financial market even further along.

Inflation spurred on by the weak yen and a rise in long-term interest rates would both put the squeeze on people’s daily lives. It is even possible that policy measures meant to support people’s lives could conversely make things worse.

Potential of consumption tax cuts to undermine credibility of the social security system

The Fundamental Reform of the Tax System Act (2012) prescribes that “with a view toward simultaneously ensuring stable financial resources for social welfare and achieving fiscal soundness, the Government shall clarify how consumption taxes are used and raise tax rates”.

Under the FY2026 draft budget, the country’s social welfare expenditures amount to 39.1 trillion yen. Meanwhile, the amount of consumption tax revenue (national tax) is expected to be 26.7 trillion yen, which falls short of the amount of social welfare expenditures by over 12 trillion yen. At a time when it is necessary, ideally, to support the social security system by increasing the amount of consumption tax revenue, reducing taxes instead would appear to be problematic.

Consumption taxes are not “earmarked taxes”, the revenue from which must, by law, be used for specific purposes. For this reason, even if the revenue brought in from consumption taxes declines, that does not mean social welfare spending will automatically be reduced.

However, if tax cut measures reduce consumption tax revenue, which serves as a basic funding source for social welfare programs, it could lead to uncertainty among the public that in the future, it might be impossible to maintain the country’s social security system, or their pension benefits or other social welfare benefits might be significantly cut. In other words, it could potentially undermine trust in the country’s social security system. If that happens, the public might become more worried about the future, and this could have an adverse effect on their spending habits as well.

It also needs to be reconsidered why consumption taxes are treated as a basic funding source for social welfare. Now, in a sense, the revenue from consumption taxes has relatively little volatility compared to those from corporate taxes or personal income taxes, and thus is well suited to be a stable funding source to cover social welfare programs, which are steadily on the rise each year. Moreover, there is also the principle which says that it is only right that the social security system – as a pillar of the welfare state – should be supported by a wide range of generations working together.

If consumption taxes were to be cut substantially, then social welfare programs would increasingly have to be covered by corporate taxes and personal income taxes. It would be odd for the corporate sector to be primarily responsible for funding the social security system, and if it were to be financed by revenue from personal income taxes, then the burden would fall squarely on working generations.

A truly drastic inflation measure would be a comprehensive tax and social security system reform

Furthermore, 59% responded that the consumption tax rate should be maintained in order to secure steady fiscal resources, surpassing the 31% who answered that the rate should be lowered even if it meant issuing deficit-financing bonds.

During the lower house elections, which would decide the country’s future and the administration’s framework, what the parties perhaps should have debated more was not a consumption tax cut – which is only a temporary measure against high prices – but rather a comprehensive reform of the tax and social security system, such as an “earned income tax credit”, which would enable the government to respond flexibly to environmental changes like rising prices and thereby support low- and middle-income earners.

The historic high prices seen these past several years have dealt a serious blow to households, especially to low- and middle-income earners. I believe the core problem is that Japan’s tax system, social security system, and wage-setting system in the corporate sector have failed to respond flexibly to high prices. For this reason, what is needed now are drastic reforms for overhauling those systems.

One of those reforms would be to introduce an earned income tax credit, a move supported by many of the country’s political parties. That would arguably be a flexible framework for protecting the real disposable incomes of low- and middle-income earners from environmental changes like future price fluctuations, and for supporting their livelihoods.

In the course of the lower house elections, instead of debating the differences among the parties’ proposals for cutting consumption taxes, there should have been a deeper debate over comprehensive reforms of the tax and social security system, including an earned income tax credit. Going forward, I hope to see the discussion over such systemic reforms pick up steam.

The parties should discuss medium- and long-term growth strategies

If we assume that an “earned income tax credit” for protecting the livelihoods of low- and middle-income earners from high prices and other environmental changes is a key “defensive policy”, then a growth strategy would function as an “offensive policy”. The important thing is to actively advance economic policies with these two approaches as the drivers.

Yet unfortunately, this kind of growth strategy was not the subject of any substantive discussions in the lower house elections. The Takaichi Administration has been advocating a growth strategy focused primarily on “crisis-managed investment and growth investment”. I would have liked to see the parties debate the pros and cons of that approach more.

The Takaichi Administration’s “crisis-managed investment” calls for the government to make larger investments in order to address various problems such as natural disasters, military threats from abroad, risks to the stable procurement of energy and food, and the risk of overseas export restrictions on essential commodities. This approach is aimed at increasing the growth rate, leading to increased tax revenues, and thereby improving the country’s fiscal environment, and within this philosophy there is even the kind of optimistic outlook that seeks to “turn disaster into opportunity”.

In actuality, there are concerns that government investment will be inefficient and highly wasteful and will likely lead government debt to increase. Further, if the government seeks to spur on industrial growth through investment, subsidies, and so forth, the corporate sector could become more dependent on the government, which potentially could hinder innovation.

Moreover, crisis-managed investment aims to bring heavy industry back to Japan, from the perspective of economic security. However, such an initiative would be geared toward substituting imports with domestic goods on an extensive scale, and in a sense could conceivably impede free trade, which is a hallmark of Japan’s national policy.

If cheap, high-quality products from overseas are replaced with domestic products, that will lead production costs to rise, leading to higher prices. And it is the Japanese people who will have to buy those products at higher prices than before.

It is the private sector and its companies, after all, that ought to play the leading roles in the economy. The government would do better to play a supporting role, aiding corporate activity from the sidelines. Ever since the Abe Administration, the growth strategies that have been propounded by successive administrations called for deregulation, measures to address the declining birthrate, and labor market reforms as ways of inducing companies to make capital investments with the aim of achieving higher growth potential and productivity growth rates. Yet the growth strategy being touted by the Takaichi Administration is centered on expanding government investment and thus differs in substance from the growth strategies followed up until now.

What I would like to see from the Takaichi Administration – which is focusing on demand-side economic policies in the form of expanding government investment – is for it to direct its attention more toward policy measures that emphasize the supply side, namely the traditional model of growth strategies.

At any rate, my hope is that in the wake of the lower house elections, the ruling and opposition parties will have deeper discussions about these “defensive policies” and “offensive policies” alike.

Profile

-

Takahide KiuchiPortraits of Takahide Kiuchi

Executive Economist

Takahide Kiuchi started his career as an economist in 1987, as he joined Nomura Research Institute. His first assignment was research and forecast of Japanese economy. In 1990, he joined Nomura Research Institute Deutschland as an economist of German and European economy. In 1996, he started covering US economy in New York Office. He transferred to Nomura Securities in 2004, and four years later, he was assigned to Head of Economic Research Department and Chief Economist in 2007. He was in charge of Japanese Economy in Global Research Team. In 2012, He was nominated by Cabinet and approved by Diet as Member of the Policy Board, the committee of the highest decision making in Bank of Japan. He implemented decisions on the Bank’s important policies and operations including monetary policy for five years.

* Organization names and job titles may differ from the current version.