On February 28, 2026, the U.S. and Israel launched a military offensive on Iran. Fears that these attacks could impede the supply of oil in the Middle East led global oil prices to spike, and WTI oil futures prices briefly rose from around $67 per barrel before the offensive to as high as nearly $120 per barrel on March 9. There are concerns that soaring crude oil prices could cause Japan’s inflation rate — which had finally begun to show signs of falling — to rise once again, leading to adverse effects on people’s daily lives.

Potential closure of the Strait of Hormuz is a source of concern

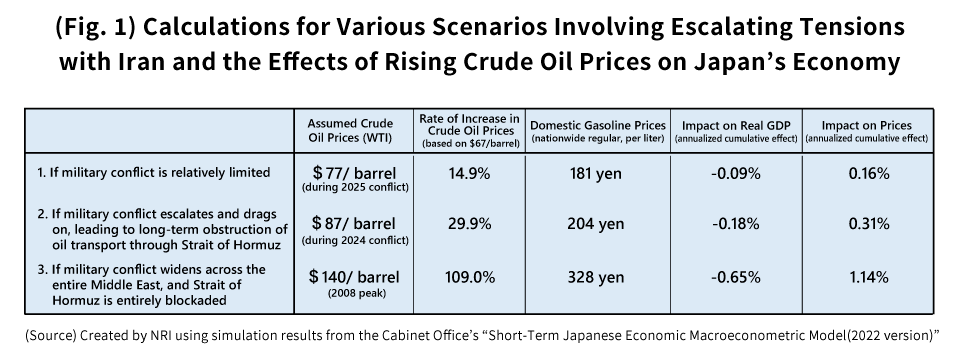

Three prospective scenarios for crude oil prices, and their effects on Japan’s economy

In the first one, the military confrontation between Iran and the U.S. and Israel would remain relatively small in scale, on par with the last such conflict in June 2025, and as happened back then, the increase in crude oil prices (WTI oil futures prices) would be only around $10 per barrel, with crude oil prices staying at around $77 per barrel.

In the second, the military confrontation between Iran and the U.S. and Israel would drag on, with the entire Middle East at risk of military conflict. In this case, I envision that while Iran would not blockade the Strait of Hormuz entirely, military actions in the region would lead the transport of crude oil to be impeded for a longer period of time. Furthermore, we could expect to see crude oil prices hover at around $87 per barrel, which was the peak they reached back in 2024 when Iran and Israel were exchanging direct attacks with each other.

The third scenario has Iran officially and entirely blockading the Strait of Hormuz, a move which could be expected to last as long as six months to a full year. In this case, the price of crude oil could jump to as high as $140 per barrel, which was the highest price it reached in 2008 prior to the financial crisis, and it could be expected to remain at that price level.

The first is an optimistic scenario, while the third is pessimistic, and the second is the base scenario (or main scenario) which I believe at present is most likely to happen.

Under this second, base scenario, I calculate that Japan’s real GDP would be depressed by 0.18% over the course of one year, with prices being pushed up by 0.31% on an annual basis. As a result of this price increase, the burden on multi-person households would rise by an annualized 11,690 yen.

In this scenario, domestic gasoline prices would go up by approximately 30%, with the average price of regular gasoline nationwide exceeding 200 yen per liter. Any downward pressure on gasoline prices from abolition of the provisional gasoline tax rate would be lost. Electricity and gas prices would also begin to rise around two to three months later as well, creating headwinds in people’s lives.

In the third scenario, Japan’s real GDP would be depressed by 0.65% over the course of a year. My calculations show that prices would be pushed up by an annualized 1.14% as well. In that event, Japan would experience a more intense stagflation with deteriorating economic conditions and soaring prices, and the chance of falling into a moderate recession would likely rise.

Domestic gasoline priced at 204 yen, electricity prices to rise to 792 yen per month, 9,508 yen for the year

First, gasoline prices will go up. If crude oil prices increase by approximately 30% in line with the base scenario, gasoline prices can be expected to go up by nearly the same percentage, reaching 204 yen per liter. It takes an oil tanker coming from the Middle East around three weeks to make it to Japan, but given that oil sellers rapidly reflect the price of crude oil overseas in their gasoline retail prices, the prices at the pump will start to rise in around one week after crude oil prices go up, and in about one month’s time the price pass-throughs will be nearly complete. If the yen continues to depreciate in the exchange markets, then the rise in domestic gasoline prices will be even greater.

Second, electricity and gas bills will rise. Electricity bills tend to go up at around 20% of the rate at which crude oil prices rise, while gas bills usually rise by 20-30% of that rate. However, it can take around three to four months for the rise in crude oil prices overseas to lead household electricity and gas bills to increase.

If crude oil prices increase by around 30% following the base scenario, then electricity bills could be expected to go up by about 6%. Currently, the cost of electricity per household is a monthly 13,219 yen on average, which works out to an annualized 158,628 yen (in 2025, from the Ministry of Internal Affairs and Communications’ “Household Survey”), and this rise in electricity costs would come out to a monthly 793 yen, or to 9,518 yen on an annualized basis.

Third, commodity prices would moderately rise for around half a year. For products that use crude oil as a raw material, the price increases will happen gradually but steadily. This means plastic containers and packaging materials, synthetic resin products, chemical fibers (nylon, polyester, etc.), paints, adhesives, and detergents, and so forth.

Even in the case of products that do not use crude oil directly as a raw material, in industries where a lot of fuel and electricity are used in the manufacturing process, the rise in crude oil prices will lead to higher manufacturing costs, and that increase will readily be passed on to product prices. That includes iron, aluminum, and non-ferrous metal products, cement and glass, chemicals, and fertilizers, for example.

Higher gasoline prices will bring about a rise in transportation costs, which will also be passed on to the prices of everyday items and foods at retail stores.

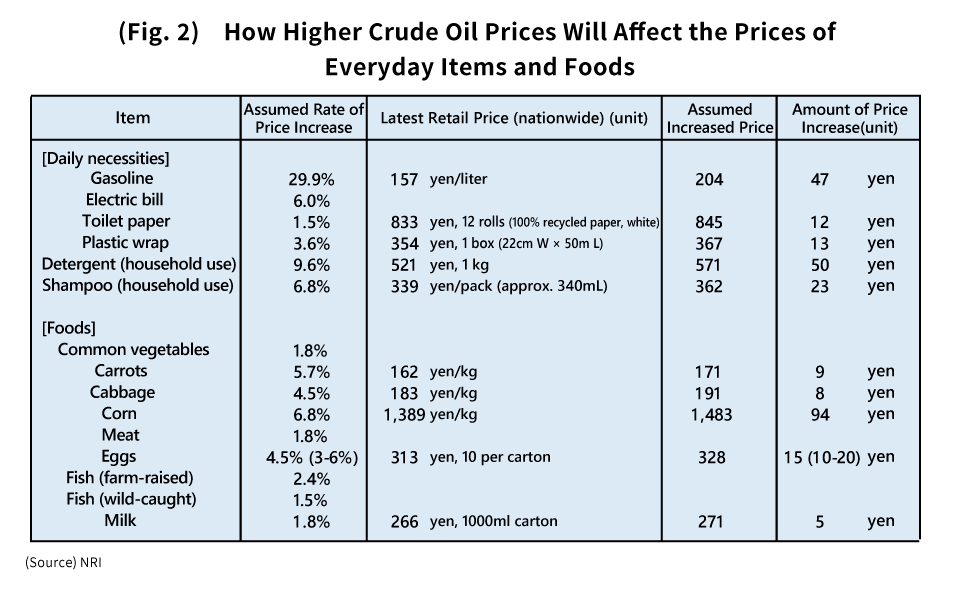

Expected impacts on the prices of individual everyday goods and foods

The figure below envisions what will happen under the base scenario, looking at the extent to which the prices of everyday necessities and foods that are staples in people’s lives will rise if crude oil prices increase by around 30%, based on the results from a statistical analysis of actual historical data (Fig. 2).

With regard to everyday items, the prices of products that directly rely on oil for their manufacturing will likely increase significantly. The price of laundry detergent can be expected to rise by 9.6%, and that of shampoo by 6.8%. The price of plastic wrap can also be expected to go up by 3.6%.

Meanwhile, even though it does not make direct use of oil as a raw material, toilet paper — which uses a lot of electricity for drying etc. in its manufacturing process — can be expected to go up by around 1.5% in price.

Foods like vegetables, meat, egg, and fish may not directly involve the use of oil as a raw material, but even still, they will be affected by the rising price of crude oil. That is because: firstly, the higher electricity costs involved in their production processes will be passed on to product prices; secondly, higher prices for chemical fertilizers made from crude oil or LNG will be passed on to product prices; and thirdly, increased transportation costs resulting from higher gasoline prices will also be reflected in product prices.

The prices of common vegetables and meats can both be expected to go up by around 1.8%, but we can infer this to be mainly a reflection of higher transportation costs (the third reason). Conversely, eggs and farm-raised fish, which require a great deal of electricity to be produced, can be expected to see proportionately significant price rises. Moreover, the prices of carrots, cabbage, and corn will be substantially higher, and this can be attributed to the impact from higher prices for chemical fertilizers used in their cultivation.

Thus, the conflict in Iran — a country geographically distant from Japan — may very well have a major impact on Japanese people’s daily lives as the rising price of crude oil broadly pushes up the prices of everyday necessities and foods.

Profile

-

Takahide KiuchiPortraits of Takahide Kiuchi

Executive Economist

Takahide Kiuchi started his career as an economist in 1987, as he joined Nomura Research Institute. His first assignment was research and forecast of Japanese economy. In 1990, he joined Nomura Research Institute Deutschland as an economist of German and European economy. In 1996, he started covering US economy in New York Office. He transferred to Nomura Securities in 2004, and four years later, he was assigned to Head of Economic Research Department and Chief Economist in 2007. He was in charge of Japanese Economy in Global Research Team. In 2012, He was nominated by Cabinet and approved by Diet as Member of the Policy Board, the committee of the highest decision making in Bank of Japan. He implemented decisions on the Bank’s important policies and operations including monetary policy for five years.

* Organization names and job titles may differ from the current version.