AI, especially generative AI has revolutionized a wide range of industries in recent years.

In this white paper, we explore the use of generative AI for risk management in the context of central counterparties (CCPs). We examine generative models that can handle and generate numerical data used in the world of finance.

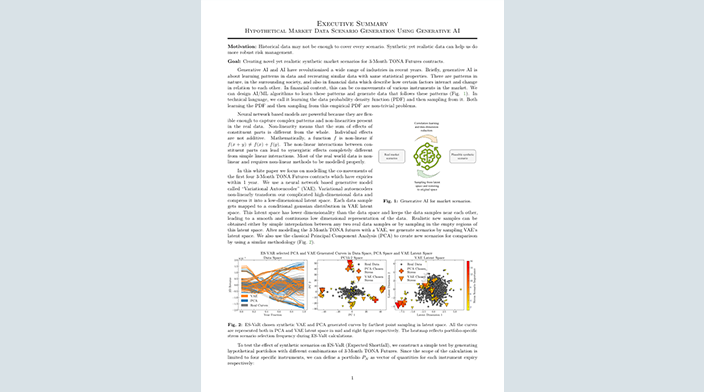

We explore how to use generative AI models to create market data with a focus on 3-month TONA Futures contracts. We compare variational autoencoder (VAE) with principal component analysis (PCA) and analyze the generated scenarios. Subsequently, we use the generated data to estimate the risk profiles of various portfolios by calculating Expected Shortfall and Value at Risk (ES-VaR).

The results show that the VAE-generated scenarios were more diverse and affected the ES-VaR more than the PCA-generated scenarios.

Hypothetical Market Data Scenario Generation Using Generative AI(Executive Summary)

Hypothetical Market Data Scenario Generation Using Generative AI(Main Report)

Author Information

-

- Author

- Minoru Aoki

- Department

- Capitai Markets Solution Business

Department

Expert

-

- Author

- Syed Hashim SHAH

- Department

- Japan Securities Clearing Corporation Aurora Solutions K.K.

-

- Author

- Joel VIKLUND

- Department

- Japan Securities Clearing Corporation Aurora Solutions K.K.